Use our LLC Operating Agreement template to identify your business as a limited liability company and establish how it will operate.

Updated August 20, 2024

Written by Josh Sainsbury | Reviewed by Brooke Davis

A limited liability company (LLC) is a type of business structure that combines the benefits of a corporation with the tax benefits of a sole proprietorship or partnership.

LLCs minimize the personal legal accountability of their members — especially in the event of litigation. It also protects the members’ assets from collection, creating a separate property from the LLC.

A business cannot receive these benefits and protections without such a document. These agreements organize the LLC and set forth essential responsibilities and obligations.

This document governs the operations of an LLC with only one member (owner).

This agreement is for LLCs with two or more members, each of whom holds a membership interest in the company.

Used for a formal change that governs which sections of the original LLC Operating Agreement will be modified or removed or new areas to be added.

An LLC Operating Agreement is a critical legal document that outlines a limited liability company’s ownership and member duties. The agreement sets out the financial and working relations that suit the specific needs of the business owners.

It is crucial to your company, from daily operations to what would happen if a member needs to leave the business. It should be created as soon as you form your limited liability company.

An agreement for a limited liability company also includes details such as:

Most states do not specifically require an Operating Agreement to create a limited liability company. However, you are afforded fewer protections without one, and a court could find that your business is not a properly formed LLC. This could result in personal liability for the LLC’s members.

| Alabama - § 10A-5A-1.08 | Montana - § 35-8-109 |

| Alaska - AS 10.50.095 | Nebraska - § 21-110 |

| Arizona - § 29-3105 | Nevada - NRS 86.286 |

| Arkansas - § 4-32-405 | New Hampshire - § 304.C:41 |

| California - Corp Code 17701.10 | New Jersey - § 42-2C-11 |

| Colorado - § 7-80-108 | New Mexico - § 53-19-19 |

| Connecticut - § 34-243d | New York - § 417 |

| Delaware - § 18-101 - § 18-1109 | North Carolina - § 57D-2-30 |

| Florida - § 605.0105 | North Dakota - § 10-31.1-13 |

| Georgia - Title 14, Chapter 11 | Ohio - § 1705.081 |

| Hawaii - § 428-103 | Oklahoma - § 18.2012.2 |

| Idaho - § 30-25-105 | Oregon - § 63.057 |

| Illinois - 805 ILCS 180/ | Pennsylvania - § 8916 |

| Indiana - IC 23-18-4-4 | Rhode Island - § 7-16-22 |

| Iowa - § 489.110 | South Carolina - § 33-44-103 |

| Kansas - § 76-7672 | South Dakota - § 47-34A-103 |

| Kentucky - § 275-180 | Tennessee - § 48-206-101 |

| Louisiana - RS 12:1319 | Texas - § 101.052 |

| Maine - § 31-1521 | Utah - § 48-3a-112 |

| Maryland - § 4A-402 | Vermont - 11 V.S.A. § 4003 |

| Massachusetts - Chapter 156C | Virginia - § 13.1-1023 |

| Michigan - § 450.4308 | Washington - RCW 25.15.018 |

| Minnesota - § 322C.0110 | West Virginia - § 31B-1-103 |

| Mississippi - § 79-29-123 | Wisconsin - Chapter 183 |

| Missouri - Wyoming - § 17-29-110 | |

| Show More Show Less | |

A written operating agreement protects a company’s limited liability status by proving the limited liability company is a separate legal entity. Without it, a company may appear to be a sole proprietorship or partnership for tax and lawful purposes.

Banks, lenders, investors, and professionals often ask for an LLC Operating Agreement before allowing a company to open a business checking account, secure financing, receive investment money, or obtain proper legal and tax help.

Your state’s default rules will apply if you do not have an agreement. For example, suppose you do not detail what happens when a company member leaves or dies. In that case, the state may automatically dissolve your limited liability company based on its laws.

If you want something different than your state’s de facto laws, an LLC Operating Agreement allows you to retain control and flexibility on how the company should operate. LLC members own a percentage of the company, not shares of a corporation.

However, state default rules often assume that each owner has an equal share of the company, even though they may have contributed different amounts of money, property, or time.

LLC Operating Agreements allow you to:

Most joint ventures established in the US are formed as LLCs for tax purposes. If you want to create your LLC as a joint venture, you might also need a joint venture agreement.

Here is a chart of consequences a limited liability company and its members may face without a written agreement.

| Individual Member | Company | |

|---|---|---|

| Loss of Time | All members must vote on both big and small company decisions | Subject to state default laws that may change or be amended without notice |

| Loss of Money | Taxed as an individual business owner instead of as an LLC member | Taxed as a sole proprietorship or partnership instead of as a company |

| Uncertainty | Unclear whether an individual is liable as a member |

An LLC Operating Agreement should include essential details about the business’s daily operations. It should generally include details about the following:

In addition to these crucial details, an adequately drafted agreement should include other valuable details like:

The first information you fill in is the names of each member of the LLC. It should include their legal name, not informal designations or “nicknames.” This legally identifies who owns the LLC, so a proper legal assignment of the parties is essential.

a) Date the agreement is being entered into

b) List the full legal names of the members entering into this agreement. In an LLC, a member has ownership and voting rights within the company.

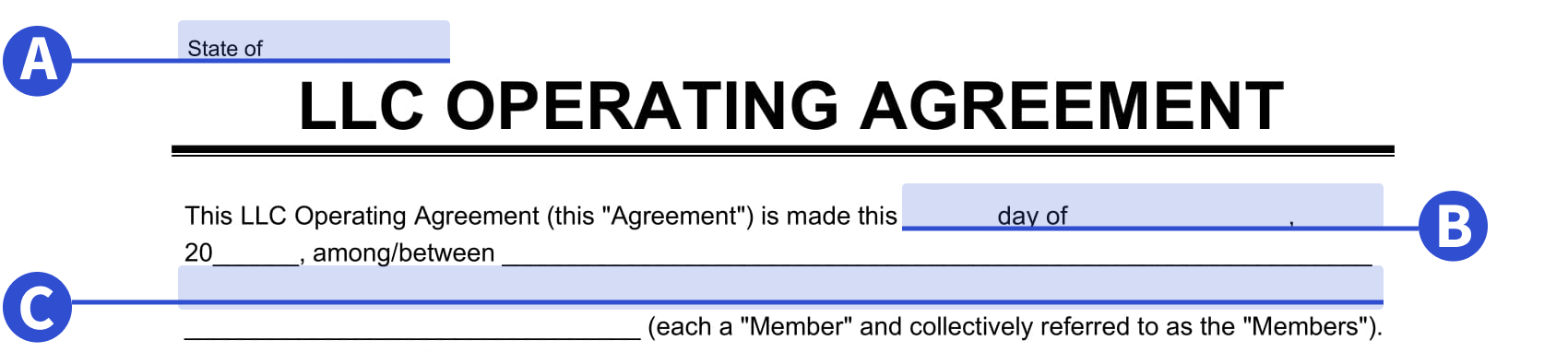

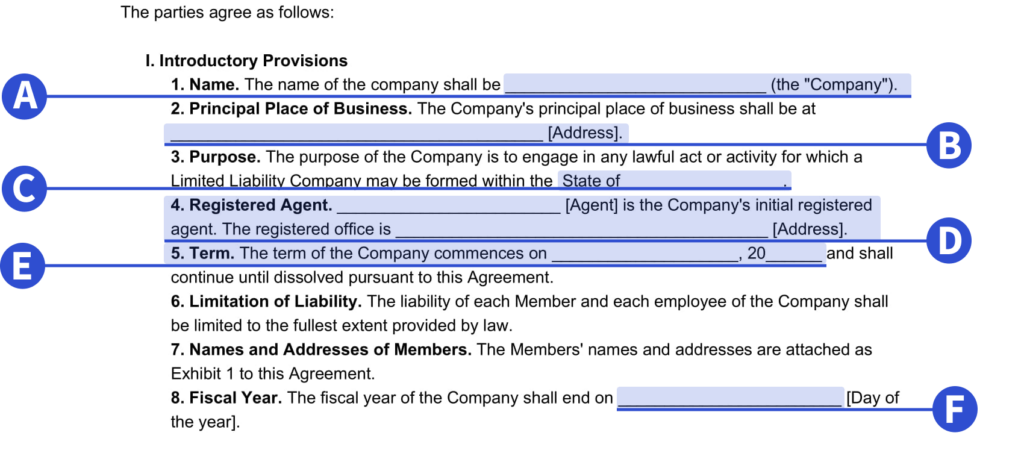

The introductory provisions set forth important summary details of the LLC Operating Agreement. It includes the company’s name, principal place of business, and purpose. It will also include information on the company’s registered agent and that person’s address.

This section should also include information on the following:

a) List the legal name under which you will operate and file taxes. This may or may not be your name for marketing or other purposes. However, this should be the name you used to file the LLC in your state legally.

Be aware that states have specific requirements for how you name your LLC. This varies by state, so be sure to check with your Secretary of State or the equivalent business formation office in your state for the naming requirements of your LLC.

b) List the legal name under which you will operate and file taxes. This may or may not be your name for marketing or other purposes. However, this should be the name you used to file the LLC in your state legally.

Be aware that states have specific requirements for how you name your LLC. This varies by state, so be sure to check with your Secretary of State or the equivalent business formation office in your state for the naming requirements of your LLC.

c) List the state or states where the LLC is registered and operating.

d) The registered agent is the designated individual or company physically located within the state who can receive service of process or other correspondence on behalf of the LLC. A member in the state can be appointed to serve as a registered agent for the LLC.

The registered office is the complete physical address of the registered agent, where service of process or other legal or official correspondence can be delivered or served upon the company. This cannot be a PO Box.

e) This is the date when the LLC officially begins operations. This may or may not be the same date as the date on the agreement.

f) This is the timeframe that the LLC will follow to establish an entire year. Most businesses follow the calendar year, which runs from January 1 through December 31; however, you can choose a different time frame as long as it is a full year. For example, your fiscal year can run from April 1 through March 31.

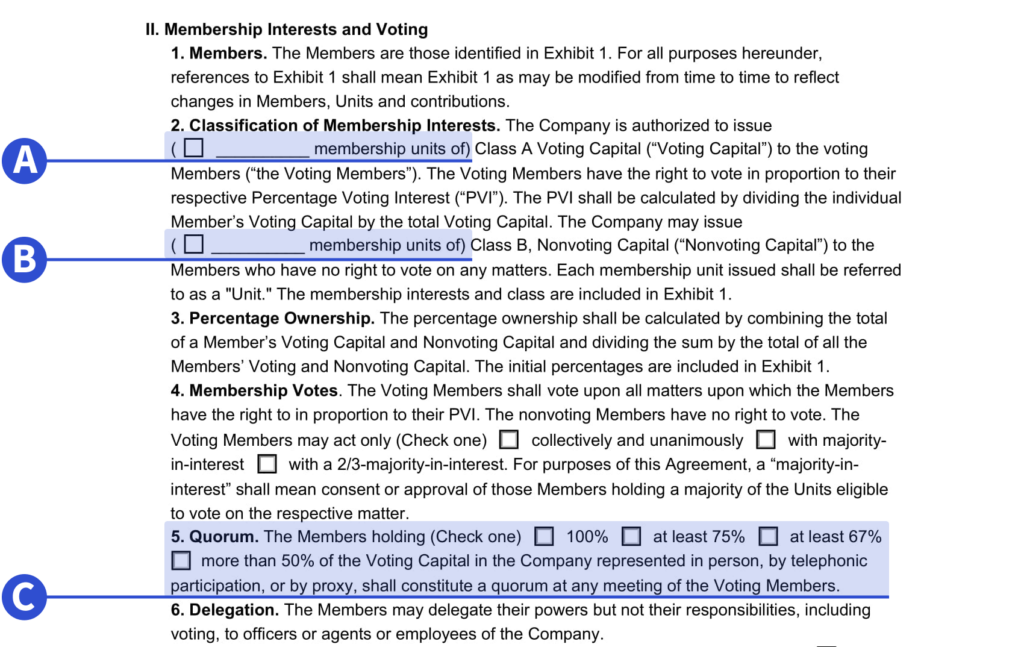

The following section will identify important information about the members’ ownership interests and voting rights.

LLCs can structure ownership rights and voting rights together or separately. This depends on how you want voting rights to work within your new company.

It will contain detailed information about voting and whether voting rights may be transferred between members. This section should also address how new members may be added and their voting rights upon becoming a member. Creating clear rules in this section may prevent significant conflict in the future.

a) This is the number of Class A units the LLC may issue its members.

b) If more than one class of membership units will be issued, you can input the number of Class B units the LLC may give to its members here.

c) The refers to how many voting members are necessary for a quorum for a meeting of members. A quorum refers to the minimum percentage of units that must be represented for an appointment to proceed.

This is not based on the number of people but rather on the number of units represented by those people. Member units are not necessarily equal.

For instance, you may elect for there to be 50% for a quorum. Bob and Sue each own 10%, less than the required 50%; therefore, if only Bob and Sue are present, you do not have a quorum. Alternatively, Jay could hold 70%. In that case, Jay alone is a quorum.

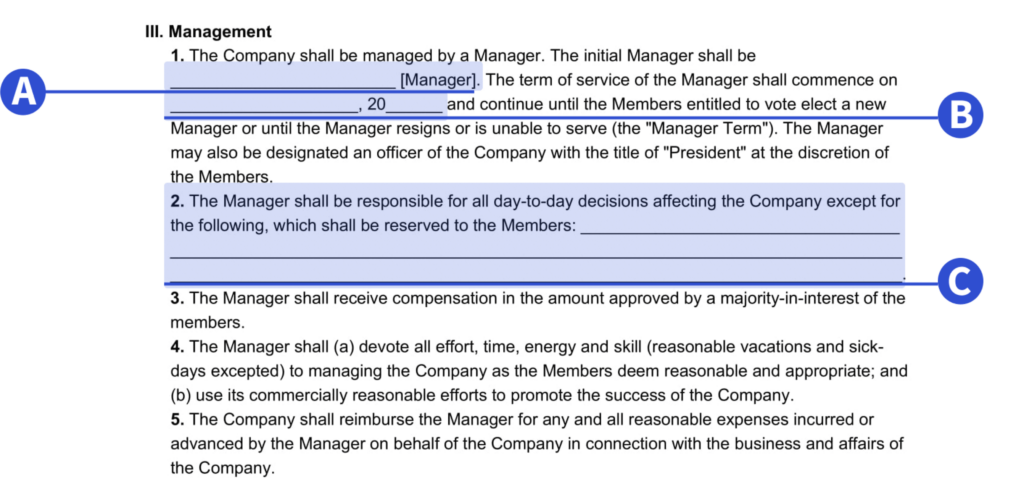

If the LLC is manager-managed, this section should detail which LLC member is the manager, the manager’s term, and how a manager is voted into their position. It should also outline the manager’s duties and rights to agree on behalf of the LLC. If applicable, it should also include any additional compensation for being a manager.

The management section will outline the manager’s duty to devote reasonable effort, time, and energy into managing the company as the members deem fair and appropriate. It should include reimbursement procedures if the manager incurs reasonable expenses on behalf of the company.

a) Manager-managed LLCs are granted authority to manage day-to-day operations but aren’t given all member authorities. A manager-management structure is preferable if the members would instead take a passive investor role in the business.

This structure may also be better if the members are not skilled in management or if the LLC is large enough to the point where it’s no longer practical to involve all members in every decision.

b) This is the date the company will begin being managed by the manager.

c) List any day-to-day decisions that only the members and the manager cannot make independently.

Capital contributions are the amount of property, services, or money each member gives in forming the limited liability company and what they may be asked to give in the future. LLC Operating Agreements should outline the members’ contributions and how they relate to their respective ownership interests.

Certain agreements may grant ownership interests without a monetary capital contribution. When this is the case, the value of the member’s contribution should be clearly stated in the agreement.

Lastly, the section should include information on if and when the return of capital contributions may occur. Outlining this information now is vital to form your new LLC adequately.

The LLC Operating Agreement should account for how net profits or losses will be determined and how they will be distributed between the members. This is typically based on ownership percentage or different ownership brackets.

A template allows you to create an allocation scheme that fits your company’s needs. It will also discuss when distributions will be made and any prerequisite conditions necessary before distributions will occur.

The compensation section should outline how the organization will account for its expenses and whether individual members may be reimbursed for their expenditures. It will also address the salary of any member or officer within the company.

The compensation section may also outline how voting will occur to determine these issues.

This section of the LLC Operating Agreement should include essential details about the following:

This section outlines how and when the LLC will cease to operate. It outlines who decides to dissolve the LLC, voting rights, and any automatic dissolution conditions like death or bankruptcy. It will also detail the specific procedures for liquidating company assets, payment of obligations, and full accounting related to winding up the business.

A well-drafted form agreement then outlines how remaining liabilities or assets are distributed to members of the LLC.

Company dissolution and liquidation is often a contentious time for a company. With clearly listed details in this section, you can seek to avoid any legal disputes on how the company should be dissolved.

a) This is the number of members required to approve a dissolution or liquidation. This number will be listed as a percentage of the membership

Indemnification provisions protect individual members from liability in several circumstances. It holds that the individual member should not be responsible for damages related to good-faith actions on behalf of the company.

These provisions also require the company to repay the individual member if they should sustain any expense or injury on behalf of the company, absent fraud, gross negligence, or willful or wanton misconduct.

Indemnification sections also typically include insurance information. This section permits the LLC to purchase and maintain insurance for the company, its members, employees, and property.

A confidentiality section outlines any information that shall not be made public, including:

These secrets often represent a substantial value to the company and require protection. This section will outline how this information must be protected, by whom, and the possible penalties for a breach. It can also set forth confidentiality exceptions for situations that require disclosure.

a) This is the state where arbitration would occur. Generally, this will be the state where the LLC was initially formed.

b) This is the state in which the LLC was formed.

With this free LLC Operating Agreement, you can build yours by filling in the blank sections. This template allows you to create an agreement that fits your company’s unique needs.